VAT rates in the EU for foreign deliveries

Prize question: Since the VAT.reform in the EU with the practical abolition of delivery thresholds, which topic has increasingly come into focus for many online traders?

No, it is not (anymore) the registration and participation in the One Stop Shop procedure. But it has to do with it.

Answer: The top issue among internationally active online traders is increasingly the reliable determination and application of the correct (reduced) VAT rates for deliveries to private customers in other EU countries.

This is because after exceeding the new EU-wide threshold (of only EUR 10,000 net in total), traders must tax their shipments to private customers in other EU countries (= “distance sales”) in the respective destination country at the tax rates applicable there.

And, let’s be clear, in many EU countries there are several different tax rates for different product groups.

Even though the actual local tax messages can be handled administratively with relative ease centrally with the OSS procedure, the OSS does not solve the underlying problem:

First of all, traders need to find out the correct VAT rates for all their goods shipped abroad in the EU and apply them. Otherwise, there is a risk of declaring and paying too little tax (tax evasion / tax avoidance) or too much tax (narrowing of the sales margin) due to incorrect tax rates.

We want to explain the following in this article:

- When and for what do traders need to know and apply the (reduced) tax rates of the EU destination countries of their supplies?

- Where are the concrete risks when tax rates are determined incorrectly?

- What solutions can be found to ensure that the correct VAT rates are applied?

Other countries, other tax rates

If you sell goods via marketplaces such as Amazon, eBay or even your own webshop within Germany, most of you hardly have to worry about which VAT rate you charge your customers.

Things get complicated when you sell your goods across borders.

Value Added Tax is now the most important source of revenue for most EU states. It is therefore understandable that correct taxation is of paramount importance for all states.

The vast majority of traders know that different tax rates apply in other EU countries than in Germany. But the right way to deal with this is often not really clear.

The fundamental question is then often first:

- Can I apply German tax rates for deliveries to private customers in other EU countries?

The answer to this is simple: No, as soon as you have reached or exceeded the new very low threshold of 10,000 EUR net for the total of your EU deliveries, you have to apply the VAT rates of the respective destination country.

Until mid-2021, this was even more differentiated, as you could pay tax on EU deliveries at the German tax rates until you reached country-specific delivery thresholds (EUR 35,000 to EUR 100,000 per country).

The follow-up question follows very quickly:

- If my goods are taxed at a reduced rate in Germany, does that also apply in other EU countries?

Unfortunately, the answer to this question is not a simple YES! Details follow below.

And finally, the king question:

- How can I find out the foreign (reduced) tax rates for my goods and then reliably apply them after the determination, especially for tax returns?

We also deal with this in detail below.

To say one thing in advance: The initial determination of the EU tax rates means some work. However, the correct application thereafter can then be automated in the long term and thus also be reliable.

Tax rates in Germany

In Germany, essentially only two tax rates are applied:

- the standard tax rate of 19 per cent, and

- the reduced tax rate of 7 per cent

The standard tax rate

Basically, you will apply the standard tax rate in Germany to most of your goods and services in the area of e-commerce. This is 19 per cent. However, there are exceptions to the standard tax rate.

The reduced tax rate

The purpose of the reduced tax rate of 7 per cent in Germany is to subsidise certain goods and services. However, there is no clear system as to which services or goods are to be subsidised.

In the e-commerce sector, the reduced rate is likely to apply mainly to the supply of foodstuffs and certain food supplements.

It becomes much more complex when you send goods across borders in the EU and you have to pay tax on your sales at the rates applicable in other EU countries. How can this happen?

Subject to VAT in other EU countries?

In cross-border e-commerce trade within the EU, there are basically three conceivable cases in which you, as a German trader, become liable for VAT in other EU countries and thus the foreign tax rates apply:

- You use foreign warehouses, e.g. within the framework of the fulfilment programme of Amazon (FBA). In this article we explain what you need to consider in this case.

- Your deliveries to private individuals in other EU countries exceed the new threshold of EUR 10,000 net in total for all countries, which is the successor regulation for the previous country-specific delivery thresholds as of 1 July 2021.

- You register for the OSS procedure, waive the threshold value by registering and thus generally pay tax on all cross-border supplies to private individuals in the EU at the tax rates of the respective destination country.

Now you know in which cases you have to settle with the foreign Value Added Tax . But how high is this exactly in individual cases?

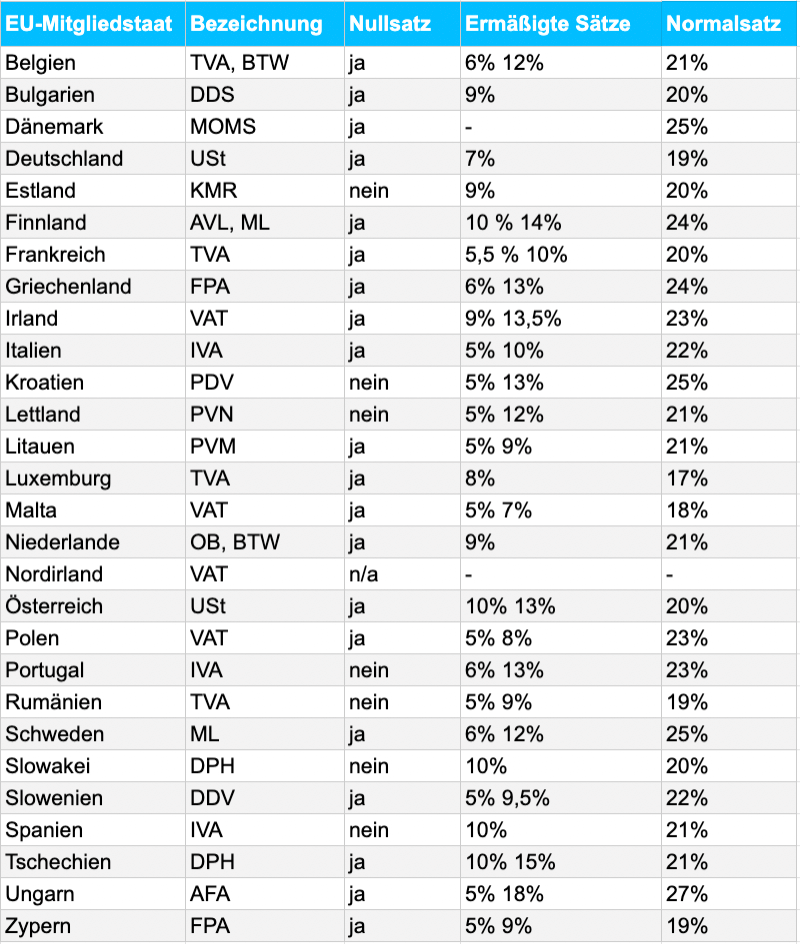

The level of VAT rates in EU countries is very diverse

There are also standard and reduced tax rates in other EU countries. The total range of VAT rates in the European Union is between 0 per cent and 27 per cent. Member States are allowed to set the following tax rates so far:

- Standard tax rate: This must be at least 15 percent. There is no upper limit.

- Reduced rate I: This must be at least 5 per cent and less than 15 per cent. The application is limited to goods and supplies listed in Annex III of the VAT Directive (page 69).

- Reduced rate II: The same restrictions apply as for reduced rate I.

- Special tax rates: Special tax rates may only be applied in exceptional cases and after approval by the EU Commission. These may even be lower than the basic lower limit of 5 per cent.

- Zero tax rate: Some Member States subject certain benefits to a tax rate of 0 percent. This should not be confused with a tax exemption, as “genuine” tax exemptions often do not allow for deduction of input tax on the corresponding input services. In the case of zero tax rates, there is therefore a double subsidy, since in these cases the trader has a right to deduct input tax.

In some countries there is even an additional so-called intermediate tax rate. This is often applied to certain wines and energy products and therefore does not play a major role in e-commerce.

Overview: Table of VAT rates in EU countries

Currently (as of 01.07.2021), the following VAT rates apply in the EU countries:

In some EU countries such as France, Spain and Ireland there are also the special tax rates already mentioned above, which are also known as super-reduced tax rates and represent special cases of the European VAT regulations.

Which VAT rate applies to your products in the EU countries?

Now you have an overview of the VAT rates in the countries of the European Union. But which tax rate actually applies to your products when they are delivered to other EU countries?

In many cases, it can be said that if the standard tax rate applies in Germany, this also applies to your products in most other EU countries.

Unfortunately, there are also numerous exceptions. For example, children’s clothing is taxed at 19 per cent in Germany. In Luxembourg , these goods are subject to a reduced tax rate of3%.

It gets even more complicated when you consider goods that are taxed at a reduced rate in Germany, such as coffee. Then you have to ask yourself in many EU countries which of the reduced tax rates from the table above applies.

Tax rate determined incorrectly! What are the risks?

If you always use the lowest reduced tax rate, you shorten Value Added Tax. If you always use the highest reduced tax rate, or even the standard tax rate of the respective country, you unnecessarily give away margin and market share.

Ignorance is no defence against punishment, even in the case of tax evasion / tax avoidance due to tax rates that are set too low, in addition to tax back payments, depending on the EU state, there are sometimes very high fines for your company. This can threaten the very existence of your company.

Conclusion: The tip that can be read from time to time, e.g. in Amazon seller forums, to always tax EU shipments at the standard tax rate “to be on the safe side” may help in the short term. In the long term, however, this is not really expedient due to the possibly considerable lost profits.

Therefore, you should always apply the correct tax rates. But the question is, when at the latest do you need to know the tax rate of your products? Until now, the answer to this question was: at the latest when issuing the invoice, as the invoice to the end customer also had to show the tax rate of the destination country in the case of cross-border deliveries.

Is this still the case with the introduction of the One-Stop-Shop?

Does the VAT rate have to be on the invoice? No obligation to issue an invoice when using the OSS procedure!

For domestic deliveries, you are used to showing the VAT rate and amount on invoices as required by law.

A special feature of the One Stop Shop procedure is that traders do not have to issue an invoice for cross-border deliveries to private individuals in the EU.

Thus, as an OSS participant, you do not have to determine, calculate and display the applicable tax rate – purely for invoicing purposes.

But don’t rejoice too soon:

At the latest for the quarterly OSS reports, you will have to assign the correct VAT rates for all articles of your deliveries, as well as calculate the taxes for each EU country and report and pay them via the OSS.

So the question arises as to how you can get to grips with the issue of tax rates and what you absolutely have to bear in mind in practice.

So which items belong on your tax rate checklist?

Without automation, effort and error-proneness increase considerably

For the compilation and evaluation of the transaction data for the EU tax returns, it is almost indispensable that you use an automated solution. This is the only way to ensure that:

- You always apply the current VAT rate to each of your goods (because tax rates in the EU change from time to time).

- Short-term tax rate reductions are automatically taken into account accordingly

- Your transaction data is prepared reliably and with reasonable effort for tax and financial accounting purposes.

This is where the use of intelligent software, such as the cloud-based VAT platform from Taxdoo, can provide you with automated support.

Taxdoo knows all sales tax rates in the EU

Taxdoo can automatically determine the current tax rate for each product and each EU country based on the customs tariff number.

From the automated transaction-based data extraction from marketplaces, webshops and all relevant ERP systems, the compilation of all data for the OSS reports, to the reports to the tax offices in other EU countries and the transfer of the data to the financial accounting system (e.g. DATEV):

With Taxdoo, online traders or their tax advisors receive everything from a single source and on the basis of coordinated automated processes.

Simply click here to arrange a live demo with our Value Added Tax and e-commerce experts, where we will personally explain the advantages of our automated Value Added Tax solution to you and/or your tax advisor via screen transmission.

Weitere Beiträge

VAT in the Digital Age – The Next VAT Reform for E-Commerce?

One-Stop-Shop (OSS) EU VAT for E-Commerce

VAT identification number and country of origin for Intrastat reporting: New requirements from 2022