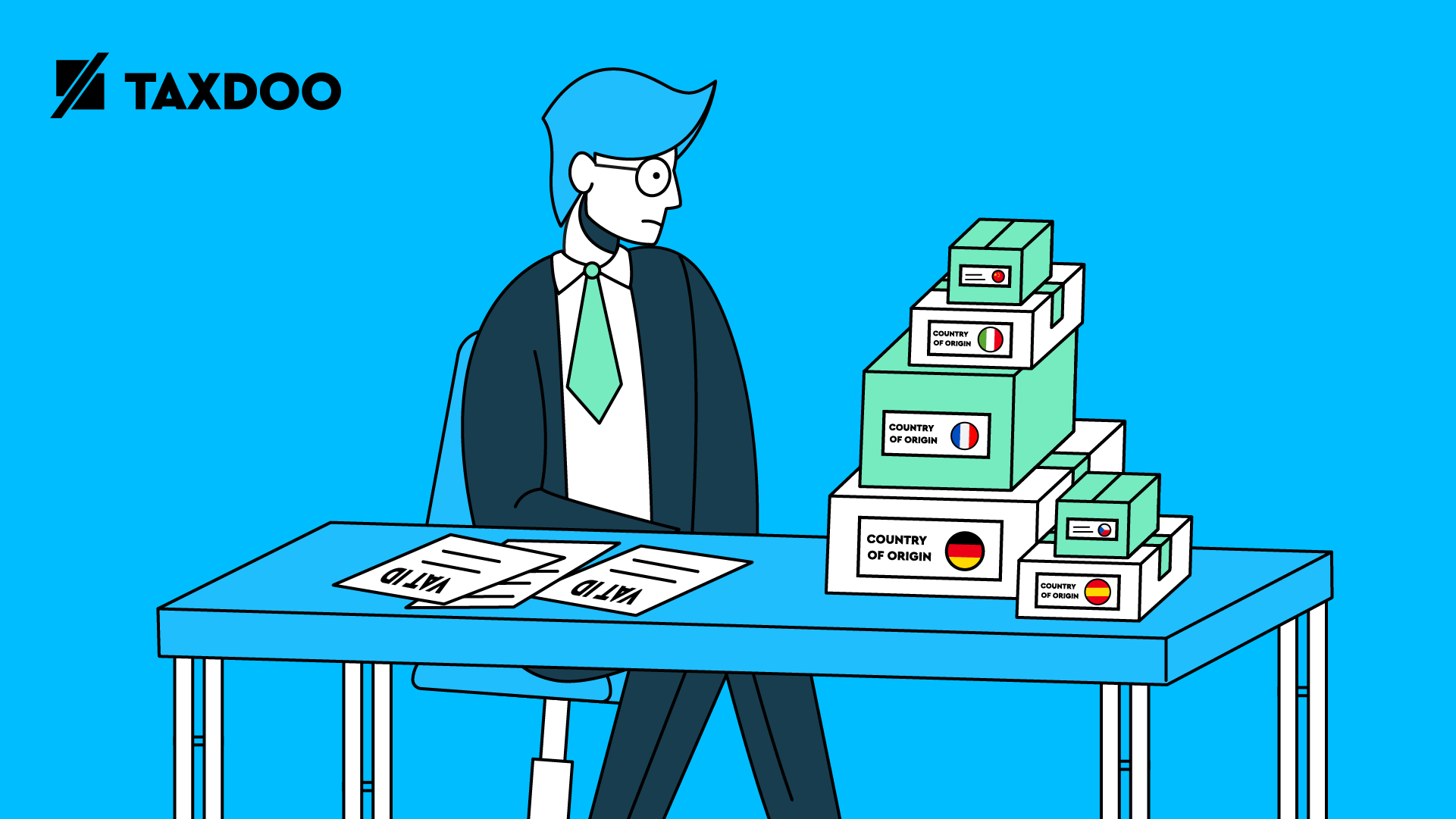

VAT identification number and country of origin for Intrastat reporting: New requirements from 2022

As of January 2022, there will be changes in the reporting of intra-trade statistics. A comprehensive report on the changes, where they come from and what you as an online merchant need to be aware of is explained in our blog post ‘Intrastat – Changes from 2022’. In this article, we would like to clarify the details of the two new requirements in the German Intrastat dispatch report. This is because, as simple as the changes sound, there are a few points you need to consider.

Which Intrastat regulations will be affected from 2022?

In Germany, there is certain information that can currently be voluntarily submitted by declarants. However, two of these fields will become mandatory for your future Intrastat declarations:

- The country of origin of goods

- The VAT identification number of the recipient

In a selection of EU countries, this information has already been made compulsory. In Germany, this will now also be the case as of January 2022.

In the following post, we will explain the most important aspects of these two new specifications.

What is the ‘country of origin’ for Intrastat declarations?

The country of origin of goods in the context of Intrastat is not the country from which you ship the goods. Instead, the origin of goods is determined by where the goods were wholly obtained or manufactured. In the case of further processing, the decisive factor is where the last significant processing took place.

Above all, you must not confuse the country of origin with the country of departure from where the goods are sold. Of course, in some cases it may be the same country. However, if you send your goods from a warehouse, in many cases the country of origin will be different from the country from which you send your goods.

Example:

If you buy your goods from a manufacturer in China, the country of origin is China. With regard to the Intrastat this means: If you sell this product from a warehouse in Germany to a private end-customer in the Netherlands, you must enter the code ‘CN’ in the field for country of origin in your German Intrastat dispatch report.

In addition to the country of origin, as of 2022 it will also be necessary to state the VAT identification number in Intrastat declarations. There will also be additional special features to consider here, which we will explain to you below.

The VAT identification number in Intrastat

Stating the VAT identification number may sound simple at first, however, this is unfortunately not always the case.

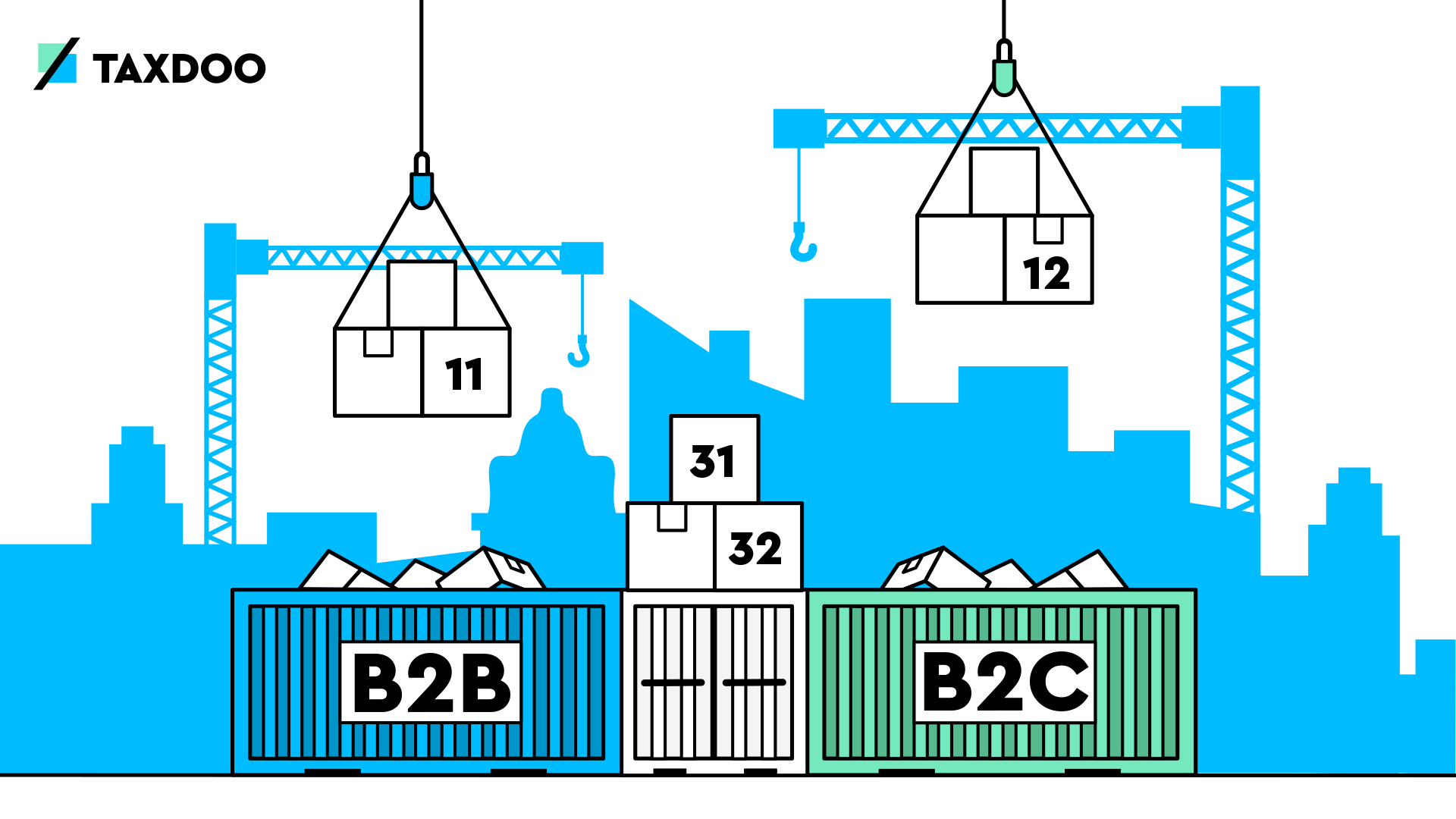

Starting in January 2022, there will be a distinction included in the Intrastat declaration between B2B turnover and B2C turnover. This is where the first question arises:

Which VAT identification number do I enter when I send my products to a private customer in another EU country?

So far, the Federal Statistical Office has no clear guideline:

If the recipient is a private person, the fictitious number QN99999999 should be entered.

However, it is not as clear as it seems. The Federal Statistical Office has concretised this issue in the Guide the Intra-Community Trade Statistics 2022, which was published (in German) in December 2021. This is because the fictitious number is not always to be taken into account when selling to private individuals.

Important:

Those who have already researched the changes in Intrastat reporting will probably not yet know these details. Until now, the Federal Statistical Office had published a guide and detailed explanations on the changes from 2022. This did not yet contain all the details of the new requirements for the VAT identification number. In particular, the dependence on OSS usage was not apparent from these documents. Therefore, there may be need for adjustment.

Intrastat: VAT ID for B2C sales depends on OSS usage

The new guideline of the Federal Statistical Office now focuses on merchant’s OSS registration.

The decisive factor is whether you have registered for the One-Stop-Shop.

If you take part in the OSS scheme, you can use the fictitious VAT ID number QN99999999 for your sales to private individuals.

If, however, you are not registered for the One-Stop-Shop but use local registration in the respective receiving member state, you should not use this number.

You should instead use your own VAT ID number for registration in the receiving member state.

Special case: Obliged to report to Intrastat, but fall below the turnover threshold

Moreover, if your B2C sales are below the turnover threshold for distance sales, you will generally neither use the OSS nor be registered in the receiving member states. In these cases, for VAT purposes, taxation takes places in the country of departure of the goods. However, these sales must still be reported for Intrastat purposes. In this constellation, you simply act as if you were registered for the OSS i.e., you declare with the fictitious number QN99999999

Good to know:

This distinction of the VAT identification number for B2C sales is a national regulation in Germany that only affects German Intrastat declaration. In other countries, however, there is no such distinction.

VAT ID in Intrastat declarations for B2B sales and movements of goods

In the case of sales to other companies (i.e., your B2B turnover) and also your movements of goods to foreign warehouses, it becomes somewhat easier – at least with regard to the VAT identification number. In your Intrastat declaration, you are to enter the VAT identification number of the recipient, i.e., either the B2B customer or your own VAT ID in the receiving member state.

In summary: The specification of the VAT ID for the Intrastat declaration depends on the recipient and your OSS registration

When stating the VAT identification number, a distinction must be made according to whom the recipient of your sale is (B2C, B2B, or a movement of goods between warehouses) and, in the case of sales to private individuals, whether you are registered for the OSS.

You should also implement this new distinction according to official guidelines. The Federal Statistical Office is in regular contact with the tax authorities and will in future also receive information regarding distance sales you declare via the OSS scheme.

In these cases, contradictory information could lead to queries from the authorities. Therefore, implementing the requirements according to the valid deadlines is advisable and saves you time and effort down the track.

Further changes as of January 2022

It does not stop with the Intrastat changes to the VAT identification number. Another significant change concerns the field ‘Type of Transaction’. This also comes into effect from January 2022 and affects both the arrival and dispatch reports.

Here, too, are important new features for online merchants. As such, we cover the changes concerning the ‘types of transactions’ separately in our next Intrastat article. If you are obliged to submit Intrastat declarations, you should not miss it.

Taxdoo & Intrastat

Does this sound complicated? No need to worry! Our tax experts have already dealt in detail with all the changes to Intrastat reporting and can handle them completely, correctly and securely for you.

You can simply book our Intrastat add-on in your customer dashboard under the ‘Add-on’ function. If you have already activated our Taxdoo add-on for Intrastat declarations, you can sit back and relax. We provide you with Intrastat declarations with all the changes from 2022 already applied.

Would you like to learn more about Taxdoo and our Intrastat service?

Then arrange a free and non-binding demo with one of our VAT experts. We will answer any questions you may have and explain how Taxdoo can best support you and your VAT needs. We look forward to meeting you!

Weitere Beiträge

VAT in the Digital Age – The Next VAT Reform for E-Commerce?

One-Stop-Shop (OSS) EU VAT for E-Commerce

Types of transactions for Intrastat declarations from 2022: A New List